Drug Pricing Indexes: Average Wholesale Price (AWP)

Cultivating clarity in the complex world of pharmacy benefits is our mission. In this post, we take a closer look at the Average Wholesale Price (AWP), one of the most widely used reference points in pharmacy pricing. Whether you work in the industry or are simply seeking to better understand how drug pricing functions, AWP remains a foundational concept. Below, we outline what AWP is, how it is used in practice, and the nuances that shape its impact across the drug value chain.

DRUG PRICING INDEXES

2/6/20264 min read

In this Episode:

The Basics

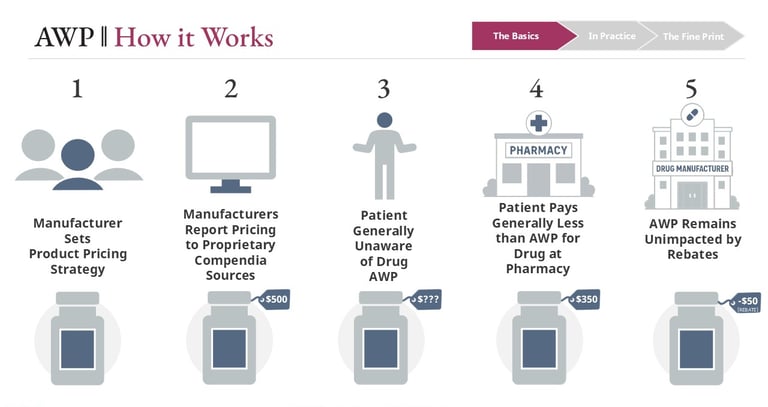

Breaking Down the Acronym

How it Works

Parallel Concepts

In Practice

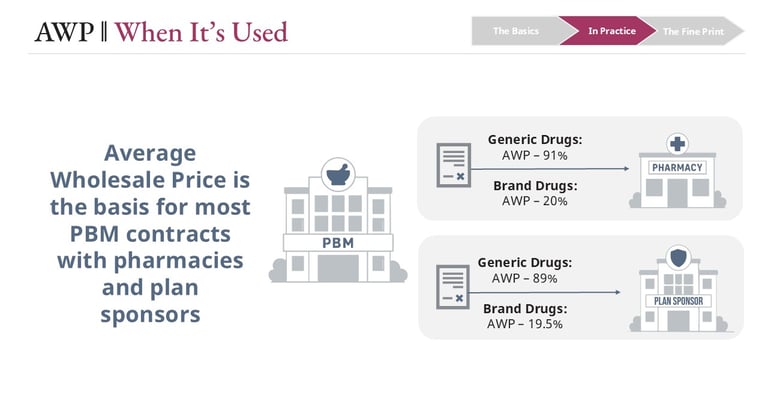

When AWP is Used

Pros and Cons

Payer Decisions

The Fine Print

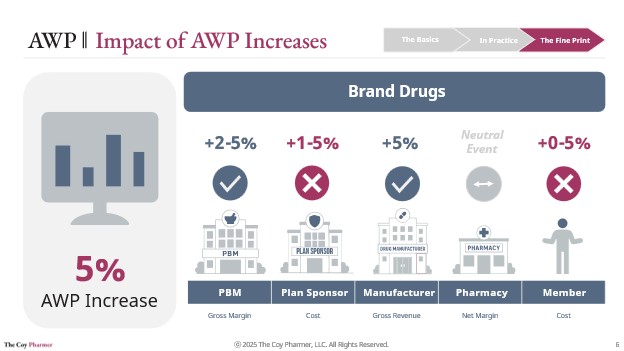

Impact of AWP Increases

The Basics of AWP

Because of its widespread use, AWP plays a significant role in financial modeling and procurement decisions. Pharmacy benefits consultants frequently rely on AWP-based projections when comparing PBM proposals, evaluating expected plan spend, and assessing the relative value of brand, generic, and specialty drug discounts alongside rebate guarantees. Small changes in AWP assumptions can materially influence projected outcomes and longer-term contracting decisions.

One reason AWP persists is its breadth and consistency. Virtually every National Drug Code tend to change gradually over time. This stability makes AWP useful for long-term modeling and contract administration, even as the index increases periodically.

Practical Applications of AWP

The Fine Print of AWP

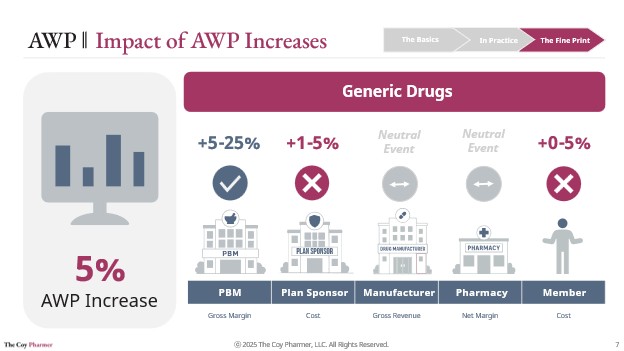

The Average Wholesale Price index has historically increased over time, with list prices for brand drugs commonly rising in the range of roughly 2 to 8 percent year over year and generic drugs increasing at a lower rate, often closer to 1 to 3 percent annually. These upward trends have complex outcomes for various players in the drug channel. Plan design, the contractual structure between pharmacy benefit managers and plan sponsors, rebate arrangements, and recent changes introduced by the Inflation Reduction Act have combined to create a complex relationship between AWP increases, margins, and net costs across the drug distribution channel.

Consistent with The Coy Pharmer’s goal of bringing clarity to this complexity, the graphics in this section illustrate some common ways AWP increases may affect different stakeholders. Member cost exposure is primarily driven by benefit design, with individuals enrolled in flat copay structures often experiencing little direct impact from AWP changes. In contrast, members covered under high-deductible or coinsurance-based plans may bear a larger share of increased costs as list prices rise.

Conclusion

While AWP may appear straightforward, it plays a central and nuanced role in the pharmacy benefits ecosystem. As a long-standing pricing benchmark, it influences contracts, reimbursement, financial modeling, and member cost exposure across the drug value chain. Understanding both its utility and its limitations is essential for informed decision-making.

At The Coy Pharmer, our goal is to make these complex dynamics more transparent and accessible. Stay tuned as we continue to examine drug pricing benchmarks, including comparisons between AWP, WAC, NADAC, and alternative contracting approaches.

Impacts to plan sponsors and pharmacy benefit managers are largely determined by the specific terms of their contracts with one another and can vary widely depending on discount guarantees, pricing methodologies, and rebate structures. The most common scenarios of AWP increases tend to derive additional margin for PBMs, with the plan sponsors absorbing cost increase. Plans and PBMs tend to include forecasted AWP increases in their internal modeling practices, to account for this common occurrence.

Pharmacy impacts tend to remain relatively neutral margin for both brand and generic drugs. For brand drugs, pharmacies typically both purchase and dispense products based on discounted AWP arrangements. This often results in relatively stable margins even when AWP changes. For generic drugs, pharmacies generally purchase on a flat unit-cost basis or may shift sourcing strategies to mitigate the effects of AWP increases. With generic drug reimbursement commonly governed by PBM-established Maximum Allowable Cost (MAC) lists, reimbursement is typically unimpacted by AWP changes. Maximum Allowable Cost is a topic with complex dynamics, which will be explored in a future post.

The AWP index is closely related to another pricing benchmark, Wholesale Acquisition Cost (WAC). In many cases, AWP is set at approximately 1.2 times WAC, though this relationship is not uniform across all products and exceptions do exist. WAC serves a different purpose in pharmacy contracting and reimbursement, and we will explore its role in a separate post.

Transitioning away from AWP is not simple. Because AWP is embedded across PBM contracts, pharmacy agreements, and plan sponsor pricing terms, shifting to a different benchmark often requires broad renegotiation across multiple parties.

At the same time, AWP has limitations. Because it is manufacturer-reported and not directly tied to observed market transactions, it can increase independently of changes in actual acquisition costs. When AWP rises, the effects can flow through benefit designs, particularly in high-deductible health plans where member cost sharing is tied to a percentage of the drug’s list-based price.

These examples reflect commercial market practice and do not capture dynamics surrounding Medicaid rebates or Maximum Fair Price in Medicare. Different benefit designs and contract structures may impact actual outcomes. These examples capture some illustrative scenarios in commercial benefits, which may not universally apply.

Average Wholesale Price remains deeply embedded in pharmacy benefit contracting. Many agreements between Pharmacy Benefit Managers (PBMs), pharmacies, and plan sponsors use AWP as the starting point for reimbursement and pricing guarantees.

For example, pharmacy reimbursement terms may be structured as AWP minus a negotiated percentage, such as AWP minus 91 percent for certain generic drugs or AWP minus 20 percent for brand drugs. Separately, plan sponsors may receive different AWP-based guarantees from PBMs, creating the framework through which PBMs manage spread, fees, and rebate arrangements.

Average Wholesale Price (AWP) is a benchmark price published for prescription drugs. While it is often referenced as a “list” or “sticker” price, AWP generally does not represent the actual price paid by pharmacies, payers, or patients. Instead, it serves as a standardized reference point for pricing and reimbursement calculations. Due to this dynamic, some in the industry joke that AWP should instead stand for “Ain’t What’s Paid.”

The AWP values are established by drug manufacturers and reported to commercial drug pricing compendia such as First Databank® and Medi-Span®. Importantly, AWP is not derived from observed wholesale transactions and does not reflect negotiated discounts, rebates, or other price concessions. As a result, AWP is commonly higher than pharmacy acquisition costs, particularly for generic medications.

A helpful analogy is the Manufacturer’s Suggested Retail Price (MSRP) in the automotive industry. Both are manufacturer-published reference prices that provide a common benchmark, even though actual transaction prices frequently differ due to negotiations, competition, and market dynamics.

Links

hello@thecoypharmer.com

© 2025 The Coy Pharmer, LLC. All Rights Reserved.