Understanding Average Manufacturer Price (AMP): A Foundational Concept in Drug Pricing

Few concepts in pharmacy benefit carry as much downstream influence as Average Manufacturer Price (AMP), yet it remains one of the least understood pricing benchmarks in the industry. For pharmacy professionals, consultants, brokers, and plan sponsors, a working understanding of AMP is essential to grasp how drug costs are established and how Medicaid reimburses pharmacies. At The Coy Pharmer, our focus is on cultivating clarity in a complicated system. As part of our Drug Pricing Index Series, this post breaks down AMP—what it is, how it is calculated, who can see it, and how it ultimately shapes both rebate economics and pharmacy reimbursement across Medicaid. By the end, you should have a practical understanding of how AMP functions inside the system—not just as a definition, but as a working mechanism.

4/30/20266 min read

In this Episode:

The Basics

Breaking down the Acronym

Parallel Concepts

How it Works

Who Can See It

In Practice

Impact on Medicaid Rebates

for Brand DrugsImpact on Medicaid Rebates

for Generic Drugs

The Fine Print

Impact of AMP Increases

AMP Relation to Generic Drug

Shortages

The Basics of Average Manufacturer Price

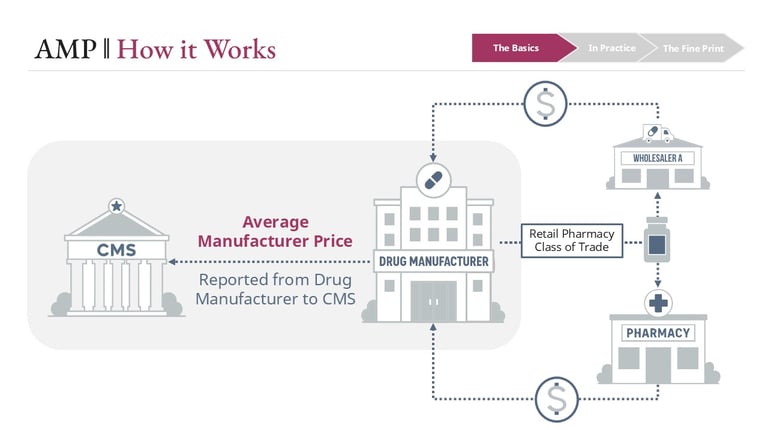

Average Manufacturer Price is the average price paid to a manufacturer for a drug by wholesalers for distribution to the retail pharmacy class of trade, along with certain direct sales to retail pharmacies. It reflects real transaction pricing within a defined segment of the supply chain—not a list price like WAC, and not a survey-based estimate like NADAC.

Manufacturers are required to report AMP to the Centers for Medicare & Medicaid Services (CMS) on a monthly and quarterly basis. These submissions are built from transactional data—primarily wholesaler invoices and direct pharmacy sales—based on strict regulatory definitions of what is included and excluded.

In Practice

The Fine Print

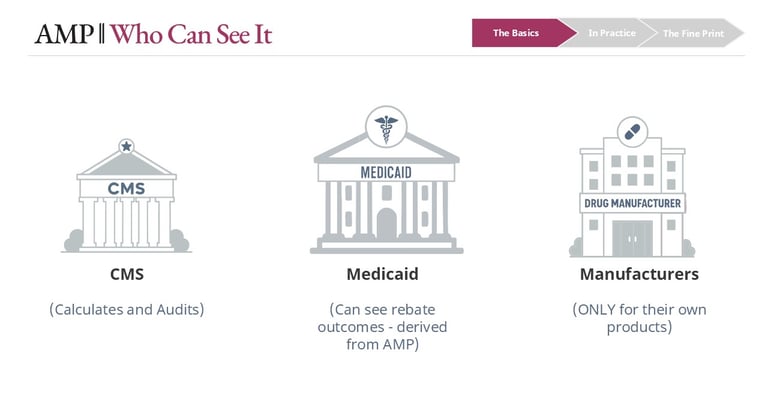

AMP is one of the most closely held data points in drug pricing. Because it reflects actual selling prices, it is considered highly proprietary. It is not publicly available, and most participants in the market—including PBMs, pharmacies, and plan sponsors—do not have visibility into AMP values.

Manufacturers can only see AMP for their own products. CMS maintains the full dataset and has audit authority over manufacturer reporting, including the ability to review underlying sales data. However, the extent and frequency of that oversight is not fully transparent.

Who can see AMP

Conclusion

Average Manufacturer Price is one of the more technical pricing constructs in pharmacy benefit, but its impact is deeply practical. It sits at the center of Medicaid rebate policy and indirectly drives pharmacy reimbursement through mechanisms like the Federal Upper Limit.

Understanding AMP means understanding how pricing decisions translate into financial outcomes across the system—from manufacturers to Medicaid programs to pharmacies.

The relationship between AMP and rebates, the role of derived benchmarks like FUL, and the timing mismatches that affect pharmacy economics are not edge cases. They are core to how the system operates.

For those working in Medicaid, PBM strategy, or pharmacy economics, AMP is not just a definition. It is part of the machinery.

What AMP actually measures

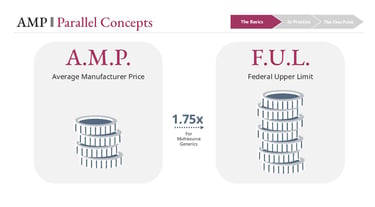

The Federal Upper Limit (FUL) connection

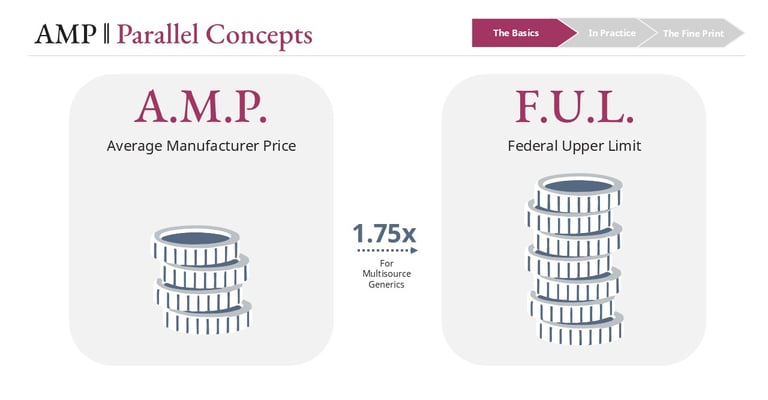

While AMP itself is not public, one of its key derivatives is: the Federal Upper Limit (FUL). The FUL establishes a ceiling for Medicaid reimbursement on certain multi-source generic drugs and is generally calculated at 1.75% of the weighted average AMP across therapeutically equivalent products.

In practice, CMS applies additional methodology and reasonableness checks, but conceptually, the FUL represents a scaled version of AMP that becomes operational at the pharmacy reimbursement level.

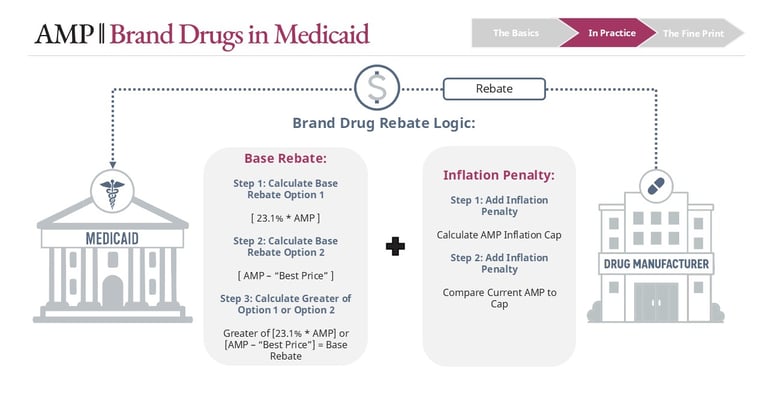

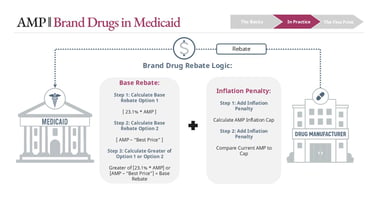

AMP and Medicaid rebates

The most important application of AMP is in calculating manufacturer rebates owed to Medicaid. These rebates differ for brand and generic drugs, and that distinction drives very different economic behaviors.

For brand drugs, the base rebate is the greater of:

23.1% of AMP, or

AMP minus Best Price

Whichever is higher becomes the base rebate. On top of that, an inflation rebate may apply if AMP has increased faster than inflation (CPI-U) since the drug’s launch baseline. That inflation rebate is added to the base rebate.

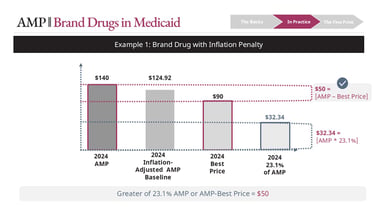

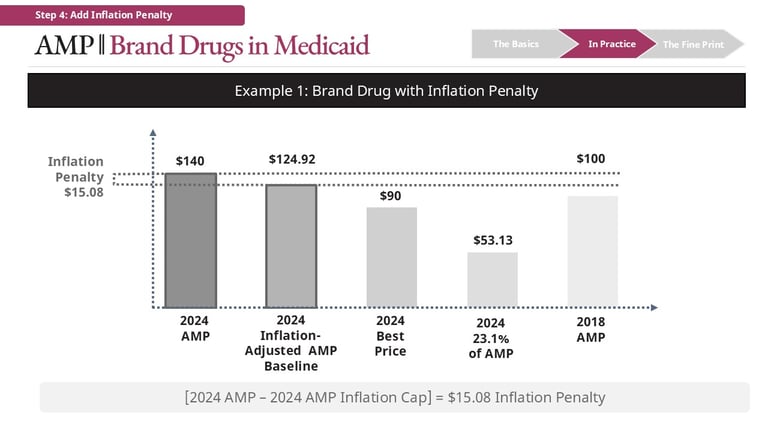

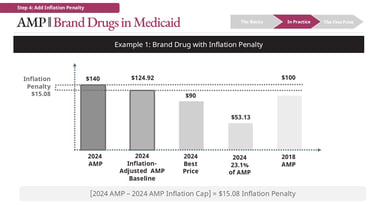

Illustrative example (brand drug)

Consider a drug with:

AMP = $140

Inflation-adjusted baseline = $124.92

Best Price = $90

The calculation for base rebate is:

23.1% * [AMP] = $32.34

Best Price = $50

Best Price > 23.1% of AMP in this case -> $50 is Base Rebate

The calculation for the inflation rebate is:

$140 [Current AMP] - $124.92 [Inflation-adjusted Baseline]

Inflation Rebate = $15.08

Total rebate = $65.08 ($50 Best Price + $15.08 Inflation Rebate)

In some cases, total rebates can become substantial relative to AMP, particularly for older brands with sustained price increases.

For generic drugs, the structure is more straightforward:

Base rebate = 13% of AMP

Plus inflation rebate (if applicable)

There is no “greater of” comparison.

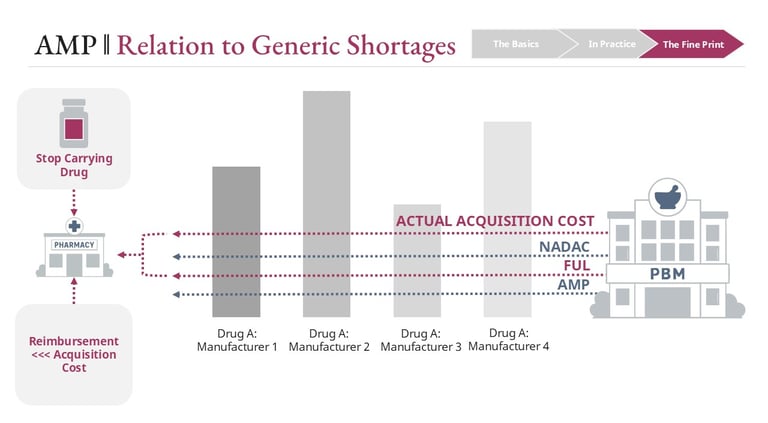

How AMP influences pharmacy reimbursement

AMP does not directly determine what a pharmacy is paid. Instead, it flows into reimbursement through derived benchmarks—most notably the

Federal Upper Limit.

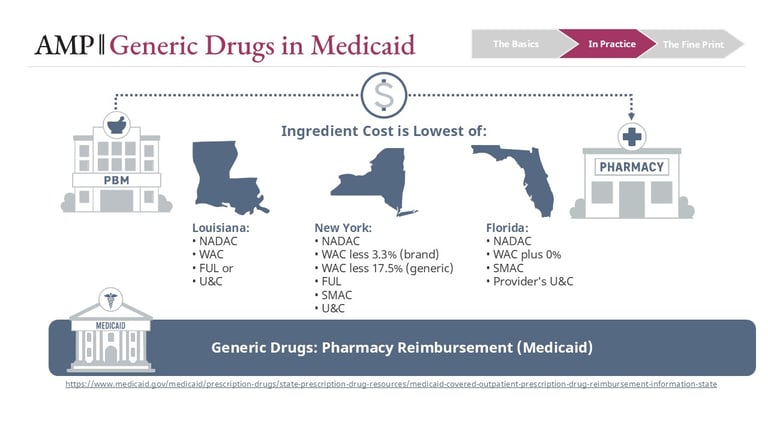

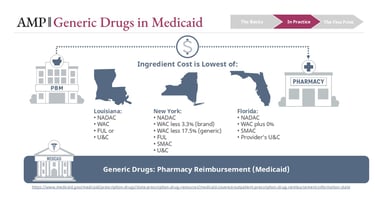

State Medicaid programs typically reimburse pharmacies using a “lower of” logic across multiple benchmarks, which may include:

NADAC

WAC-based formulas

FUL

State MAC lists

Usual and Customary pricing

This methodology is the subject of frequent legislative updates. For a better understanding of how this methodology differs by state, visit the Medicaid.gov website.

Operationally, this looks like:

PBMs administer these rules on behalf of Medicaid programs. If the FUL is the lowest available benchmark, it becomes the reimbursement basis. If NADAC is lower, it may take precedence. In some states, a state MAC list overrides both.

The result is a dynamic system where AMP indirectly—but meaningfully—shapes what pharmacies are paid at the point of sale.

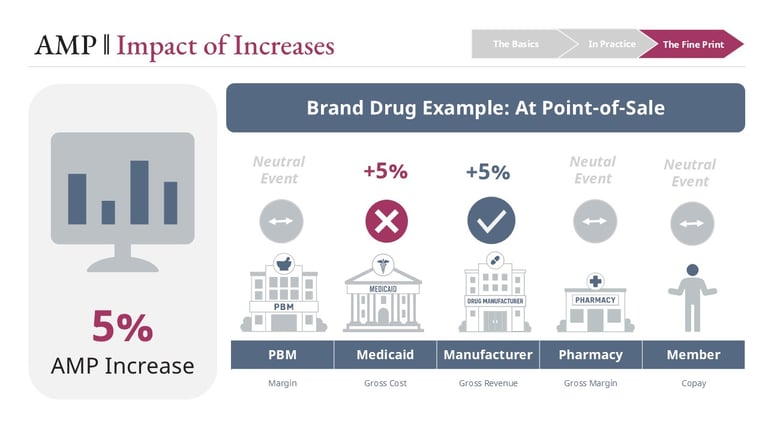

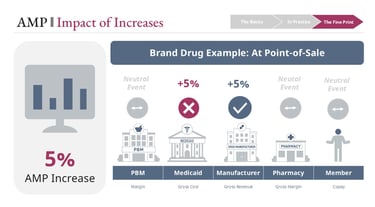

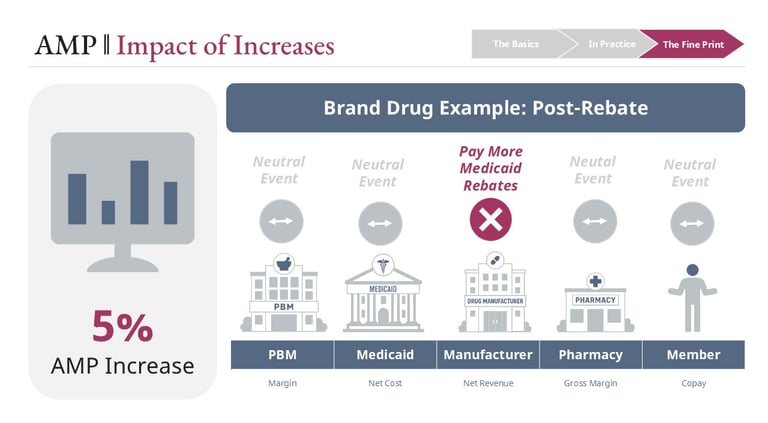

When AMP increases for a brand drug, the initial effect is straightforward: manufacturers generate higher gross revenue. Medicaid may also pay more at the point of sale. Because members often have very low or no copay in Medicaid, AMP changes do not typically impact member payments at point of sale.

The rebate system is designed to counterbalance that increase. If the price rise exceeds inflation, the inflation rebate effectively returns that incremental value to Medicaid. Because AMP also feeds the base rebate calculation, total rebates can, in some cases, offset—or even exceed—the gain from the price increase.

This is a structural feature of the system, not a flaw. It is intended to discourage rapid price escalation.

For pharmacies, the impact is typically neutral—higher acquisition costs are generally matched by higher reimbursement benchmarks. Medicaid members see little impact due to low, fixed copays.

Brand drugs: A system designed to push back

Generic drugs: where timing matters

For generics, the story is less stable. When AMP increases, the FUL will eventually adjust upward—but not immediately. There is a built-in lag between when AMP changes and when updated FUL benchmarks are reflected in reimbursement.

During that lag:

Pharmacies may be purchasing at higher costs

Reimbursement is still tied to older, lower FUL values

This creates a temporary but very real margin squeeze. Pharmacies can lose money dispensing certain generics during this window.

When system dynamics break down

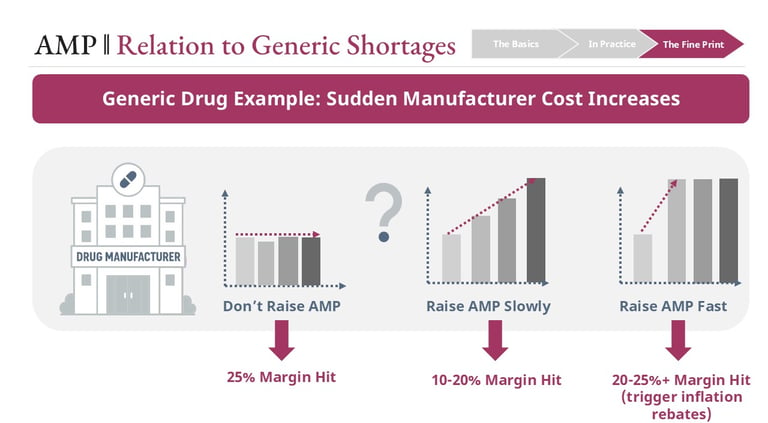

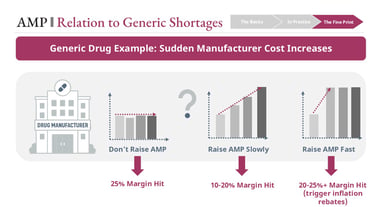

These pressures intensify when AMP increases are driven by external cost shocks rather than discretionary pricing decisions.

For example, if input costs rise sharply—due to tariffs, supply chain disruptions, or raw material shortages—manufacturers face constrained choices:

Absorb the cost and lose margin

Increase AMP gradually and partially trigger inflation rebates

Increase AMP rapidly and trigger significant rebate penalties

At the same time, rapid AMP increases worsen the FUL lag effect, putting pharmacies at risk of negative reimbursement.

When both manufacturers and pharmacies are under margin pressure simultaneously, the product can become economically unsustainable. Pharmacies may stop stocking it. Manufacturers may scale back production.

This is one of the structural contributors to generic drug shortages—not a single decision point, but an interaction between pricing rules, timing delays, and economic constraints across the channel.

Links

hello@thecoypharmer.com

© 2025 The Coy Pharmer, LLC. All Rights Reserved.